Samuel Smith and Marco Pinchetti

Recent events in the Middle East, as well as Russia’s invasion of Ukraine, have sparked renewed interest in the consequences of geopolitical tensions for global economic developments. In this post, we argue that geopolitical risk (GPR) can transmit via two separate and intrinsically different channels: (i) a deflationary macro channel, and (ii) an inflationary energy channel. We then use a Bayesian vector autoregression (BVAR) framework to evaluate these channels empirically. Our estimates suggest that GPR shocks can place downward or upward pressure on advanced economy price levels depending on which of the two channels the shock propagates through.

The channels of GPR

To assess the effects of geopolitical tensions on the macroeconomy, it is first necessary to quantitatively measure GPR. Our approach to measuring GPR follows the work of Fed researchers Caldara and Iacoviello (2022), who develop an index GPR based on the number of articles covering adverse geopolitical events in major newspapers. This index reflects automated text-search results of the electronic archives of 10 major western newspapers. It is calculated by counting the number of articles related to adverse geopolitical events in each newspaper for each month (as a share of the total number of news articles).

Chart 1 shows the behaviour of the GPR index from 1990 to 2023. The index is relatively flat during large parts of the sample, and spikes around major episodes of geopolitical tension, such as the outbreak of the Gulf War, 9/11, the beginning of the Iraq invasion in the 2000s, and the Russian invasion of Ukraine in 2022.

Chart 1: The GPR index

Source: Caldara and Iacoviello (2022).

In the same paper, Caldara and Iacoviello (2022) show that on average, an increase in the GPR index is associated with lower economic activity, arguing that these effects are associated with a variety of macro channels, ranging from human and physical capital destruction, to higher military spending and increased precautionary behaviour.

However, episodes of geopolitical tension often involve increased concerns about the supply of energy to global markets. Chart 2 shows the cumulated percentage change in the three months ahead West Texas Intermediate (WTI) futures around key geopolitical events. Oil future prices rose following most of these episodes, potentially reflecting expectations of supply cuts to energy production or disruption of the flow of energy.

Chart 2: WTI futures three months ahead prices during the 30 days following major recent geopolitical events (associated with tensions on energy markets)

Source: Refinitiv Eikon.

This suggests that GPR can also transmit via an additional energy channel, whose effects are more akin to an adverse supply shock. Whether the shock transmits through this channel, and how strong it is relative to the macro channel, will depend on the wider context and/or location of the events relating to the shock. Disentangling the two effects is, therefore, important for correctly assessing the economic consequences of a GPR shock.

Measuring geopolitical surprises

We begin our analysis by constructing a series of exogenous surprises in (i) GPR, and (ii) oil prices that can be assumed to be entirely driven by geopolitical events to a reasonable degree of approximation.

In order to construct our surprise series, we adopt a selection of 43 main GPR events from 1986 to 2020 proposed by Caldara and Iacoviello (2022), which we update to include four important events that have occurred in the past three years: the escalation of the Afghanistan Crisis in August 2021; the Russian invasion of Ukraine in February 2022; the Istanbul bombings in November 2022; and the events in the Middle East in October 2023.

We compute the GPR surprise as the daily log difference in the GPR index around these events. For the oil price surprise, we compute the daily log difference in WTI future prices from one to six months ahead around the same dates. We then take the first principal component of these to capture movements in energy prices driven by the geopolitical shock.

Decomposing the macro and energy supply components of geopolitical surprises

We then use our event-study data set in a Bayesian-VAR setting for the euro area, the UK, and the US from January 1990 up to October 2023 to disentangle the effects of the macro uncertainty channel from the energy supply channel of GPR. We adopt the two-block VAR structure proposed by Jarociński and Karadi (2020), which uses high frequency data combined with narrative and sign restrictions to identify shocks.

Within the high-frequency block, we include our surprise series of (i) log changes in the GPR index in the main geopolitical event days, and (ii) the first principal component extracted from changes in WTI futures from one to six months ahead in the main geopolitical event days, both cumulated at monthly frequency in case of multiple events occurring in one month. Within this block, we impose the sign restrictions at the core of our identification strategy, which we outline in Table A.

We impose that the response associated with the macro channel drives upward surprises in the GPR index and negative surprises in the oil future curve during the first day the news is reported, as oil prices drop following a contraction in economic activity. Conversely, we impose that the response associated with the energy supply channel drives upward surprises in the GPR index jointly with positive surprises in the oil future curve during the first day the news is reported, as precautionary oil demand rises in response to concerns about future supply cuts or shipping disruption.

Table A: The sign restrictions associated with each channel of GPR

| GPR Macro | GPR Energy | |

| GPR surprises | + | + |

| WTI surprises | – | + |

In our monthly frequency block, we include the GPR index in logs, real Brent crude prices spot in logs, real natural gas spot prices in logs (as measured by the IMF benchmark), and the monetary-policy relevant price indices in levels (in deviation from their long-run trends, as is standard in the VAR literature).

Identifying two distinct channels of GPR

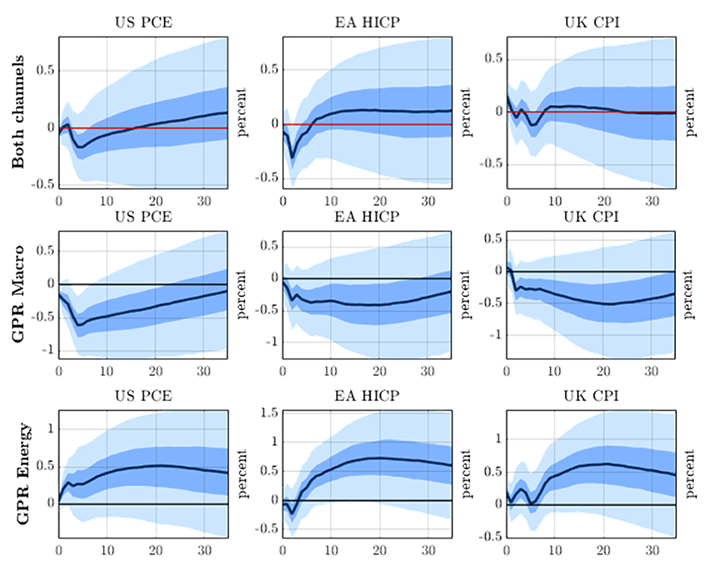

Chart 3 plots the response to a geopolitical shock that leads to a 100 basis points increase in the GPR index. The first row reports the responses of oil and natural gas prices to an ‘average’ geopolitical shock, which does not disentangle the effects of the macro and the energy channel, along the lines of Caldara and Iacoviello’s work. The second and the third rows display the responses when we assume that all of the increase in the GPR index propagates via just the macro channel and just the energy channel respectively.

Chart 3: Impulse response functions associated with an ‘average’ 100 basis points GPR shock, as opposed to a 100 basis points shock acting exclusively either through the macro or the energy channel

In the ‘average’ case, the real Brent price spot rises by about 10% on impact, before then dropping of beyond 10% after around six months. However, these dynamics mask the two underlying channels. On the one hand, the energy supply channel is associated with a rapid 20% surge in the oil price. On the other, the macro channel is associated with a more gradual decline of beyond 20%.

The response of gas prices tends to be more persistent than oil prices: the effect of the energy channel on oil prices is concentrated in the first six months whilst the effect on gas prices wanes only during the second year after the shock.

The response of price levels across regions follows a pattern that is broadly consistent with energy price dynamics. As Chart 4 shows, inflation unambiguously drops in the ‘average’ case: the price level drops persistently by about 0.1% in the US, and shortly by about 0.25% in the euro area, while the response is not statistically significant for the UK. This finding is consistent with the interpretation of Caldara and Iacoviello (2022) of geopolitical shocks behaving, from an empirical perspective, as contractionary demand shocks.

However, this similarly masks the effects of the different underlying channels. On the one hand, the pure macro channel gives rise to a more pronounced drop in the median price level than in the case of the ‘average’ GPR shock, reaching -0.5% in the US and the UK, and -0.4% in the euro area. On the other hand, the response associated with the energy supply channel is inflationary, with the price level rising persistently by about 0.5% in the US, 0.7% in the UK, and 0.6% in the euro area.

Chart 4: Impulse response functions associated with an ‘average’ 100 basis points GPR shock, as opposed to a 100 basis points shock acting exclusively either through the macro or the energy channel

Summing up

This analysis highlighted the existence of two separate and intrinsically different transmission channels of GPR: (i) a deflationary macro channel, and (ii) an inflationary energy supply channel. Policymakers should be aware of these distinct channels: GPR shocks may propagate in different manners and require different responses.

Samuel Smith works in the Bank’s International Surveillance Division and Marco Pinchetti works in the Bank’s Global Analysis Division.

If you want to get in touch, please email us at [email protected] or leave a comment below.

Comments will only appear once approved by a moderator, and are only published where a full name is supplied. Bank Underground is a blog for Bank of England staff to share views that challenge – or support – prevailing policy orthodoxies. The views expressed here are those of the authors, and are not necessarily those of the Bank of England, or its policy committees.

Share the post “The transmission channels of geopolitical risk”

Publisher: Source link

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}