Lily Smith

Like mother, like daughter? Like father, like son? Despite the increasing prevalence of digital payments in today’s world, young people continue to use cash. The persistence of cash use, even among youngsters who have grown up with debit cards and smartphones, raises interesting questions about the factors that influence young people’s payment choices. Are they really rebelling against their parents or are they more like them than they care to admit? It seems that young people are following in their parent’s footsteps and choosing to use cash because their parents do so. And instead of rolling their eyes at their advice, young people are in fact turning to them for hints and tips on money management.

In 2024, the Bank of England undertook a survey with 3,000 young people to help better understand young people’s payment behaviours and their attitudes towards cash. The survey featured a quantitative online survey with 2,000 11–17 year olds and 1,000 18–25 year olds which was nationally representative across gender, age, region, and socioeconomic background. Respondents were asked about the payments methods they most commonly use, their reasons for using cash, how they receive cash, what they do immediately upon receipt of cash, and their main sources for advice on money management.

The Bank of England conducts a bi-annual survey with UK adults aged 16+ on payment preferences which shows that, even after Covid, cash is still preferred by around 1 in 5 UK adults. However, this survey does not sufficiently capture payment attitudes of those under 16 years old. Our young people’s survey, therefore, aims to support the Bank’s understanding of future cash demand for this age demographic, helping to inform forecasting and policy decisions and ensuring that the Bank’s commitment to cash extends to all ages.

Of course, there are limitations to any survey; our young people’s survey covered only a sample of the 11–25 year-old population and was online only. We know from previous surveys conducted by the Bank that telephone respondents tend to be higher cash users than online respondents, which will likely impact which payment methods respondents say that they use most often for their day-to-day spending.

However, given that the survey met demographic quotas and results were weighted, we are confident that the results are broadly reflective of young people’s attitudes towards different payment methods. The results were also supplemented by 10 qualitative in-depth interviews, allowing us to dig deeper into the reasons behind young people’s payment choices.

Please note that the term ‘parents’ is used across this article to encompass any individual who has an influential role in a child’s life, including but not limited to relatives, guardians, and caregivers.

So what does the research show?

Cash usage decreases as children get older, with 83% of pre-teens (ages 11–12 years old), 80% of younger teenagers (13–14 years old), and 77% of older teenagers (15–17 years old) using cash. Cash use then drops off further at 18 years old. However, cash is the go to payment method for all ages from 11 to 25; overall, 80% of 11–17 year olds and 67% of 18–25 year olds use cash when making payments.

Some pre-teens expect to make the transition to card payments when they get old enough, reflecting a perception that alternative payment methods to cash might be associated with becoming a ‘grown up’.

Chart 1: Responses to the survey question: how do you pay for things?

Source: Bank of England Young People’s Attitudes to Cash Survey 2024.

Additional findings highlighted that young people in Northern Ireland and Yorkshire have the highest cash usage and male respondents are more likely to use cash than female respondents. This resonates with results from the Bank of England’s bi-annual survey of UK adults aged 16+ where preference for cash is highest in Northern Ireland, Wales, and the North East, as well as among male respondents.

There are several reasons why young people might choose to use cash, including its ease of use or usefulness for budgeting. Some mentioned using cash to ‘accommodate vendor preference’, and 22% of young people ‘just like to use it’, pointing towards more emotional drivers of cash use. For some young people, there is also a reliance on cash, with 59% of those with physical disabilities using cash as their preferred in-person payment method.

However, across all respondents, parental cash use has the most significant influence on whether a young person uses cash.

The apple doesn’t fall far from the tree…

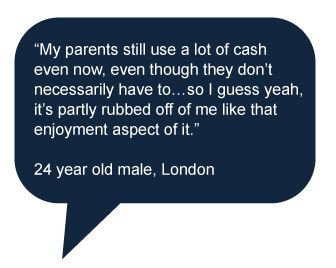

Across all ages surveyed, young people whose parents use cash say that they are more likely to use cash themselves. This pointed to both learned behaviour and the practicalities of cash use; if your parents favour using cash, you are more likely to get cash from them, and in turn use it yourself.

So what are the main ways that kids get their cash? Unsurprisingly, the standout ways are pocket money or as a gift from loved ones on birthdays or Christmas (cue the act of ‘accidentally’ missing the cash fall out of the card). 61% of 11–17 year olds and 29% of 18–25 year olds receive cash as pocket money, while 24% of 11–17 year olds and 34% of 18–25 year olds receive cash as a gift.

Chart 2: The most likely ways that young people receive cash, split by age

Source: Bank of England Young People’s Attitudes to Cash Survey 2024.

For 45% of 11–17 year olds and 21% of 18–25 year olds, the main reason they use cash is because their parents or family members give it to them, making the decision to use cash more of a passive choice rather than an active one.

The way parents handle money can also affect their children’s attitudes toward cash. If parents primarily use cash for day-to-day spending, their children say that they are more likely to adopt similar behaviours. Those whose parents are heavy cash users are also more likely to hold a higher value of cash in their purse or wallet compared to those whose parents are not heavy cash users. However, this was not expressed as a conscious choice, with young people saying that they follow these behaviours for ease or inadvertently doing what feels familiar. Perhaps they are a chip off the old block after all.

Mother knows best…

As you might expect, social media is a notable source of financial advice for youngsters. Around a quarter of young people are turning to social media as their main outlet for advice on money management, likely thanks to TikTok trends like cash stuffing and ‘influencers’. In fact, 14% of young people use TikTok as their main source of financial advice, while 27% get their financial tips from school and other educational institutions.

However, contrary to popular belief, not all young people have their heads buried in their phones, with 73% of 11–25 year olds instead turning to their parents or other family members for financial advice. While the prevalence of this decreases as respondents get older, parents are still the most common source of advice on money management for 22–25 year olds.

Chart 3: Where do young people get help on how to manage money?

Source: Bank of England Young People’s Attitudes to Cash Survey 2024.

In households where parents are open about their own money struggles or goals, young people often get their first taste of financial wisdom straight from the source. Parents from lower-income backgrounds, in particular, might stress the importance of saving, avoiding debt, and budgeting, with an emphasis on cash as a tool for staying on top of finances. A 2023 survey by Lloyds Bank similarly finds that 83% of parents agree that cash is important for their child’s understanding of finances.

Young people might also learn the value of money by receiving pocket money as a payment for doing household chores. Handling real money can help them get the hang of saving, spending, and budgeting… and also teaches them that a clean room is worth at least five pounds.

Final notes

Young people still reach for cash over other payment methods – and in large part, that’s thanks to their parents. Parents influence their kids’ financial habits through their own cash usage and by teaching them important lessons on money management. Whether intentionally or merely by example, parents are key in keeping cash relevant for the younger generation’s financial choices.

Lily Smith works in the Bank’s Future of Money Division.

If you want to get in touch, please email us at [email protected] or leave a comment below.

Comments will only appear once approved by a moderator, and are only published where a full name is supplied. Bank Underground is a blog for Bank of England staff to share views that challenge – or support – prevailing policy orthodoxies. The views expressed here are those of the authors, and are not necessarily those of the Bank of England, or its policy committees.

Share the post “Parental guidance: the influence of parents on young people and their attitudes towards cash”

Publisher: Source link

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}