Joanna McLafferty, Kirstine McMillan and Joseph Smart

On 7 May 2024 the SONIA rate, the UK’s risk-free reference rate, printed at exactly 5.2000% and has remained there to the end of July 2024 (the time of writing). Flatlining of SONIA is not a phenomenon we see often. Prior to this, over the past six years SONIA had been ‘flat’ for only four consecutive days, on two occasions. So how is it possible for the SONIA calculation methodology to create such a flat rate? What is happening in the underlying market? And most importantly… does the lack of volatility indicate an issue? We argue this should not cause concern since flatlining is explained by the calculation mechanics and behavioural dynamics in the market.

SONIA is the Sterling Overnight Index Average rate and is a measure of the rate of interest paid on eligible short-term wholesale funds in the sterling unsecured deposit market. The Bank reformed the SONIA calculation methodology in April 2018 and has produced SONIA since then. In this article we review the Bank’s methodology to understand what lies behind the flatlining observed in recent months, and whether this should be a cause for concern. So, let us take a look under the hood.

Looking behind the printed rate

SONIA is measured, as published in the Bank’s key features and policies, ‘as the trimmed mean, rounded to four decimal places, of interest rates paid on eligible sterling denominated deposit transactions. ‘The trimmed mean is calculated as the volume-weighted mean rate, based on the central 50% of the volume-weighted distribution of rates.’

This last part – ‘based on the central 50% of the volume-weighted distribution of rates’ means, by definition, if the central 50% of the volume-weighted distribution of rates is trading at one single rate, then the SONIA rate will also be that rate (Figure 1).

Figure 1: Worked example of trimmed mean methodology

Note: For illustration purposes only, it represents total volume of £1 billion. Top and bottom 25 percentiles include £250 million worth of trades.

And this is what we are seeing now. The majority of volume in the market is trading at the central rate of 5.20%. You can see this in the percentile information, published by the Bank alongside the SONIA rate, since the 25th and 75th percentiles (rates occurring at the 25th and 75th percentile of volume ranked by rate) were exactly 5.2000%, every day since 7 May. When the 25th and 75th percentiles are at 5.2000% then SONIA, as an average of the central 50% of the volume, will also be 5.2000%. SONIA will remain at this rate as long as the central 50% (or more) of volume continues to be executed at 5.2000%.

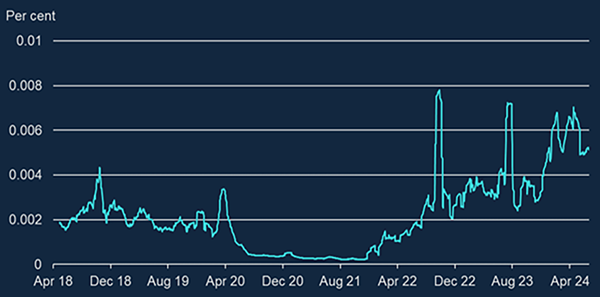

If we were to calculate a volume-weighted mean without the trimming in calculation then this would typically sit below SONIA, as shown in Chart 1. This is due to a negative skew in the underlying rates distribution since smaller trades tend to transact at lower rates. Note that SONIA is typically considered in relative terms to Bank Rate – the chart below shows the spread to Bank Rate, calculated simply as SONIA minus Bank Rate.

Chart 1: Pre and post-reform SONIA rates as a spread to Bank Rate

Despite the 25th and 75th percentiles converging and the central band of SONIA trading at one rate, there continues to be a spread of rates underpinning the SONIA market. The spread between the 10th and 90th percentiles (now around 5 basis points) has also recently narrowed but, interestingly, is not at its narrowest (Chart 2).

Chart 2: Distribution of SONIA – spread to Bank Rate

The cross-sectional volume-weighted variance of rates of SONIA trades, shown on the Chart 3 below, suggests that even though the central 50% of volume is concentrated at one rate, the rates distribution has become somewhat wider since 2021. That reflects a longer tail of transactions executed at rates away from mean.

Variance looks to have moved with the level of Bank Rate over recent years. Variance was particularly low in 2020 while Bank Rate was 10 basis points – perhaps because there was very limited space between Bank Rate and zero. As Bank Rate has increased since the end of 2021 variance has picked up, reflecting a longer tail of transactions.

Chart 3: Weighted variance of trades underpinning SONIA – 20-days moving average

To trim or not to trim

Does this raise any concerns around the trimming in the methodology?

Trimming was introduced to the SONIA calculation methodology as part of the Bank’s benchmark reform in 2018 (further information can be found at SONIA reform webpages). Pre-reformed SONIA was calculated as the untrimmed volume-weighted average. The trimmed rate was favoured due to its robustness to outliers and unrepresentative trades, and lesser sensitivity to erroneous or potentially manipulative trades. We can see from Chart 1 that without trimming, SONIA would be more volatile.

Pre-reformed SONIA was more volatile for a number of reasons including a different monetary policy environment and market conditions, the fact that the rate was based on brokered trades only (narrower coverage of the total overnight unsecured market) and – last but not least – the calculation methodology (Chart 1). Pre-reform, SONIA printed at the same rate for a maximum of two consecutive days.

Influencers, of the financial kind

What is driving this market behaviour? The changing dynamics in the SONIA market is an early effect of the process of draining reserves from the system, which has caused SONIA to drift upwards relative to Bank Rate. The SONIA market is comprised of banks (Sterling Monetary Framework) participants with access to Bank reserves (Bank of England Market Operations Guide) on the borrowing side and wholesale investors, mainly money market funds and other investment funds (with no access to Bank reserves), on the lending side. The ‘SONIA-Bank Rate wedge’ – the difference between SONIA and Bank Rate – is one indicator of the extent of abundance or scarcity of reserves in the system. When reserves are abundant, banks have little need to borrow cash in the overnight market, so SONIA typically sits beneath Bank Rate. As liquidity draining progresses, banks may have to compete more for overnight funding and lenders may be able to demand a better return on their deposits, pushing rates higher and moving SONIA closer to Bank Rate.

In April and May the SONIA-Bank Rate wedge compressed from c.6 basis points (in 2024 Q1) to 5 basis points. (And immediately following the Bank Rate change on 1 August 2024 SONIA remained exactly 5 basis points below Bank Rate). That has coincided with a period of elevated and slightly more volatile overnight sterling repo rates. SONIA is typically less volatile than the repo market since it is more relationship-driven and repo volatility is affected by collateral availability/scarcity. One explanation for SONIA being flat could be an extent of stickiness in the journey upwards in deposit rates as banks seek to resist an erosion of margin earned on this cash (for example by placing these deposits on reserve earning Bank Rate).

So to the killer question: does it matter?

SONIA plays an extremely important role in financial stability and monetary policy transmission having replaced GBP LIBOR as the main sterling reference rate. It is referenced in over £90 trillion new transactions a year. The robustness of SONIA is paramount – this is founded on the rate being based on actual transactions in a functioning and sufficiently deep market.

Flatlining of the SONIA rate for a prolonged period is unprecedented. However, since the rate continues to reflect what is happening in the market – a change in behaviour in the market affecting the shape of the distribution of rates – it is not necessarily cause for concern. Volumes in the market have been fluctuating around c.£50 billion in the months preceding this article, demonstrating depth in the market. The data suggests that the market participation remains diverse. And as we have shown above, weighted variance has actually increased despite the current concentration in the central 50% of the distribution. Taking all this together, the market is continuing to function, and SONIA is continuing to reflect the market.

Where will the SONIA-Bank Rate wedge go from here?

There are many possible drivers of activity, all of which will have some influence on volumes and rates in money markets, so we cannot make any definitive predictions. That said, the backdrop of liquidity draining means SONIA could resume its upwards drift at some point. Either way, SONIA’s recent flatlining is no cause for concern and as markets are subject to change, it could end in a heartbeat.

Joanna McLafferty, Kirstine McMillan and Joseph Smart work in the Bank’s Sterling Markets Division.

If you want to get in touch, please email us at [email protected] or leave a comment below.

Comments will only appear once approved by a moderator, and are only published where a full name is supplied. Bank Underground is a blog for Bank of England staff to share views that challenge – or support – prevailing policy orthodoxies. The views expressed here are those of the authors, and are not necessarily those of the Bank of England, or its policy committees.

Share the post “SONIA: steady as she goes”

Publisher: Source link

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}