Neha Bora, Sarah Burkinshaw, Alice Crundwell and Tuli Saha

Private equity (PE) has rapidly become an important source of financing for UK businesses. Funds use pools of capital, largely from institutional investors, to primarily invest in non-publicly traded companies. We shed light on this growing sector with a new and novel data set of around 9,000 privately backed corporates in the UK. These corporates employ over two million people, with business activity concentrated in London and in certain sectors such as information and communications. We find that they are relatively more vulnerable to default than all other corporates, and they are financed with relatively larger proportions of shorter tenor debt, like private credit and leveraged loans.

The June 2024 Financial Stability Report (FSR) details the growth in the PE sector during the period of low interest rates. Private equity funds have extended finance to companies who make important contributions to the UK real economy. For example, capital investments into PE are long-term, which incentivises PE fund managers to act less cyclically, potentially reducing the volatility of financing flows in macroeconomic downturns and improving corporate resilience. At the same time, the FSR also highlights areas of concern in the sector, particularly as we’ve entered a higher-rate environment, with sharp refinancing risks potentially on the horizon.

To shed light on the sector we created a PE data set identifying corporates with funding from private equity, private credit, and venture capital. The data set combines information on corporate balance sheets, ownership chains, and financing structures, and is sourced from a range of commercial data providers such as Preqin, Moody’s Bureau Van Dijck (BvD), and the London stock exchange group (LSEG). The rest of this post will discuss our main findings from this data set.

1. PE-backed corporates have a material real economy footprint

Using our newly created data set, we find that PE-backed corporates account for around 5% of UK private sector revenues, 15% of UK corporate debt, and around 10% of UK private sector employment – that’s over two million employees (Chart 1).

Chart 1: PE-backed corporates have material UK real economy footprint

Sources: Department for Business and Trade’s business population estimates (BPE), Moody’s BvD, Preqin and Bank calculations.

We find that PE-backed corporates tend to be larger than the average corporate in the economy, as captured in the Department for Business and Trade’s business population estimates (BPE) (Chart 2). These larger firms drive the real economy footprint.

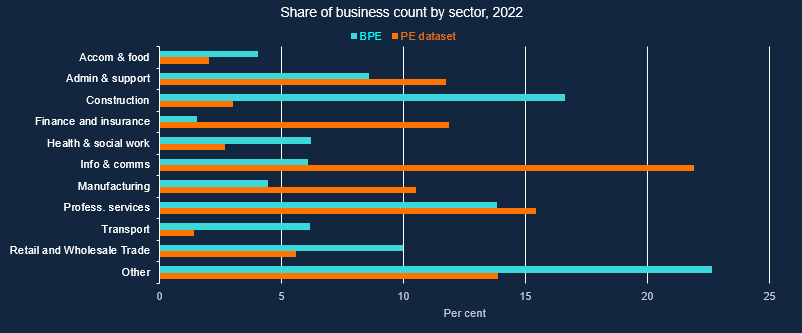

Chart 2: Business count comparison between our PE data set and BPE by size of firm

Sources: Department for Business and Trade’s BPE, Moody’s BvD, Preqin and Bank calculations.

2. PE-backed corporates are concentrated in the information and communications sector and in London

Comparing the sectoral composition in the BPE to the PE data set, we find that PE-backed corporates are more concentrated in the information and communications, finance and insurance, and professional services sectors (shown by orange bars in Chart 3) compared to the overall economy (aqua bars).

Chart 3: Business count comparison between our PE data set and BPE by sector

Sources: Department for Business and Trade’s BPE, Moody’s BvD, Preqin and Bank calculations.

Similarly, Chart 4 shows that employment in PE-backed corporates is much more highly concentrated in London. This distribution is based on company headquarters, so in practice these firms could have more of a regional footprint than this chart implies.

Chart 4: Business employment comparison between our PE data set and BPE by region

Sources: Department for Business and Trade’s BPE, Moody’s BvD, ONS, Preqin and Bank calculations.

These concentrations across sectors and geography could leave the overall PE-backed market more exposed to shocks affecting particular sectors and regions.

3. PE-backed corporates appear to be more vulnerable than other corporates

Corporates with low interest coverage ratios (ICR), negative return on assets (RoA), and a low liquidity ratio tend to be more vulnerable to default. We find that a larger proportion of PE-backed corporates simultaneously breach key thresholds for these metrics than in the respective samples for all other corporates and listed corporates. This is shown in Chart 5, which plots the liability-weighted proportions for the different types of corporates crossing thresholds of ICR below 2.5, liquidity ratio below 1.1, and a negative return on assets. However, the business model of PE can be to invest in struggling companies.

Chart 5: The vulnerable tail of PE-backed corporates is higher than other corporates

Sources: Moody’s BvD, Preqin, Refinitiv Eikon from LSEG and Bank calculations.

To gauge what drives the results in Chart 5, we break down the sample by the individual risk metrics in Chart 6. We find that PE-backed corporates have a higher share of companies with low ICR and negative RoA. Although not included in the calculations of the shares in Chart 5, we also find that PE-backed corporates have a larger share of highly leveraged firms. Offsetting this, PE-backed corporates tend to have higher liquidity than other corporates in our sample.

The increase in the risky PE tail from 2018 seems to be mainly driven by an increase in the share of firms with negative RoA. This coincides with an increase in the share of highly leveraged PE-backed corporates. Additionally, the share of PE-backed corporates with high leverage and negative RoA has fallen since its pandemic peak.

Chart 6: Metric by metric analysis shows that the peak was driven by a rise in companies with negative RoA, higher leverage, and low ICRs

Sources: Moody’s BvD, Preqin, Refinitiv Eikon from LSEG and Bank calculations.

4. PE-backed companies typically have a higher share of risky credit compared to all corporates.

Chart 7 shows that PE-backed corporates have a larger share of private credit and leveraged loans compared to all market-based corporate issuers. These instruments typically have shorter tenors than bonds, resulting in a steeper refinancing requirement for PE-backed corporates. These are also riskier forms of market-based funding and so would be sensitive to a souring in investor sentiment. Investors stepping back from these markets could therefore cause refinancing challenges for PE-backed corporates, particularly if there is limited scope to substitute with other forms of funding. Bank analysis has found that PE-backed corporates may be disproportionately exposed to refinancing risk in these riskier credit markets over the coming years. In a stress scenario, this risk could crystallise into losses for lenders.

Chart 7: PE-backed corporates use a larger share of private credit (aqua bar), leveraged loans (purple bar), and high-yield bonds (orange bar) compared to all corporates

Sources: Moody’s BvD, Preqin, Refinitiv Eikon from LSEG and Bank calculations.

While interpreting these findings, it’s important to note that our analysis is limited in several ways. We cannot be sure that we capture the whole universe of private firms – potential data gaps across vendors prevent us from forming a complete picture of privately backed companies. However, we draw comfort that our estimates are in line with what has been reported by other data vendors and market intelligence.

Summing up

Our PE data set sheds new light on PE-backed corporates in the UK, including their real economy footprint, firm characteristics, and relative riskiness. PE-backed corporates tend to be larger, more concentrated in certain sectors like information and communications, financing and insurance, and professional services sectors, which chimes with our finding that PE-backed firms are also disproportionately concentrated in London. We also find that PE-backed corporates are relatively more vulnerable to default than all other corporates, and that the PE-backed corporate debt financing structure consists of a larger proportion of shorter tenor debt, like private credit and leverage loans, which can lead to sharper refinancing needs. If investors pull back from these markets, certain firms could reduce employment and investment thereby amplifying downturns. In the extreme, these firms could also default and lead to losses for lenders.

Neha Bora, Sarah Burkinshaw, Alice Crundwell and Tuli Saha work in the Bank’s Macro-financial Risks Division.

If you want to get in touch, please email us at [email protected] or leave a comment below.

Comments will only appear once approved by a moderator, and are only published where a full name is supplied. Bank Underground is a blog for Bank of England staff to share views that challenge – or support – prevailing policy orthodoxies. The views expressed here are those of the authors, and are not necessarily those of the Bank of England, or its policy committees.

Share the post “Shining a light on private equity backed corporates in four findings”

Publisher: Source link

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}