Natalie Burr, Julian Reynolds and Mike Joyce

Monetary policymakers have a number of tools they can use to influence monetary conditions, in order to maintain price stability. While central banks typically favour short-term policy rates as their primary instrument, when policy rates remained constrained at near-zero levels following the global financial crisis (GFC), many central banks – including the Bank of England – turned to unconventional policies to further ease monetary conditions. How can the combined effect of these policies be measured? This post presents one possible metric – a Monetary Conditions Index – that uses a data-driven approach to summarise information from a range of variables related to the conduct of UK monetary policy. We discuss what this implies about how UK monetary conditions have evolved since the GFC.

What are monetary conditions?

The idea of constructing a Monetary Conditions Index (UK MCI) – a summary metric of variables related to the conduct of monetary policy – is not new.

Traditionally, monetary conditions were defined as a combination of information from short-term interest rates and exchange rates (eg Batini and Turnbull (2000)). Earlier literature on MCIs therefore typically focused on a small number of variables.

This approach has become less defensible as many central banks – including the Bank of England – extended their toolkit with a range of monetary tools. The key feature of more recent approaches to measuring monetary conditions, therefore, has been to examine a wider range of variables, in order to capture information about tools such as quantitative easing (QE) and forward guidance, which aim to influence longer-term interest rates.

Conceptually, monetary conditions don’t include risky assets or private credit. This is because they do not fall within the category of variables relating to the conduct of monetary policy, as they are likely to be affected by credit risk premia. These would be relevant for measures of broader financial conditions.

It is important to stress that monetary conditions do not provide a direct reading of a central bank’s monetary stance. The monetary stance describes the impact of policy rate today, in combination with expectations of future policy actions, on real economic activity (February 2024 Monetary Policy Report). Monetary conditions are related to, and influenced by changes in the monetary stance, but by other factors too (such as household preferences for holding bank deposits).

Methodology

Our approach for constructing the UK MCI is similar to the data-driven approaches of Kucharčuková et al (2016) and Choi et al (2022). We estimate a Dynamic Factor Model (DFM) from a combination of the policy rate – which was constrained for a prolonged period by the effective lower bound (ELB) on nominal interest rates post-GFC – with a wider range of monetary and financial variables. We extract common factors driving comovement of the variables in our data set and construct a weighted average of these factors. Weights are equal to the proportion of overall variance that each factor explains, divided by its standard deviation.

This data-driven approach avoids imposing priors on the weights (eg relating the weights to the impact of individual variables on macroeconomic outcomes), which seems a natural benchmark.

We use monthly data since 1993, after the UK adopted inflation targeting. Our data set combines both price and quantity variables and includes three main variable categories.

First, interest rates. More specifically, Bank Rate; short-term overnight index swap rates (up to three years); and long-dated gilt yields (up to 20 years). We motivate the inclusion of interest rates across the yield curve as these are directly affected by policy rates and QE purchases, and likely to contain useful information on forward guidance.

Second, we follow Lombardi and Zhu (2018) by including monetary aggregates and central bank balance sheet variables to provide further information about monetary policy operations. Following Kiley (2020), these variables enter the DFM twice, as (log) levels and as year-on-year changes, to account for stock and flow effects respectively. It is debatable whether monetary aggregates and balance sheet variables provide material additional information about the real economy effects of monetary policy, over and above their impact on interest rates (see Busetto et al (2022) and Broadbent (2023)). Though this may risk double-counting, to the extent that our modelling strategy aims to let the data speak for itself, incorporating monetary aggregates and balance sheet variables provides useful information about their comovement with interest rates.

A key question is how to treat the exchange rate. Some MCIs retain the exchange rate to account explicitly for policy transmission via this channel. While they are part of the transmission of monetary policy, exchange rates are not seen as a policy instrument by the Monetary Policy Committee (MPC), and, importantly, are influenced by many domestic and global factors which may not be informative about UK monetary conditions (Forbes et al (2018)). On those grounds, we exclude the exchange rate. Sensitivity analysis suggests its inclusion did not materially change the empirical results.

Results

To give a sense of what is driving changes in the UK MCI, Table A summarises the estimated factor loadings from the DFM, as well as the weight of each factor in the UK MCI. The factor loadings reflect how the variables are weighted together within each factor, as well as the correlation between the variables and each factor. We assign a positive sign to Bank Rate across all factors, so that increases imply tighter monetary conditions; we expect a negative sign on monetary aggregates and central bank balance sheet variables, as an expansion in these quantities implies looser conditions.

Table A: Factor loadings

Notes: Factor loadings are averaged across different subcategories of variables.

Source: Authors’ calculations.

The factor loadings suggest that all blocks of variables have a significant bearing on the UK MCI. The first factor – which explains the largest share of common variance between the variables – is mainly driven by interest rates, the stock of monetary aggregates and balance sheet variables. By contrast, the rate of change of the quantity variables is the main driver of the second factor. We retain the first three factors, which explain almost 90% of overall variance in our data set.

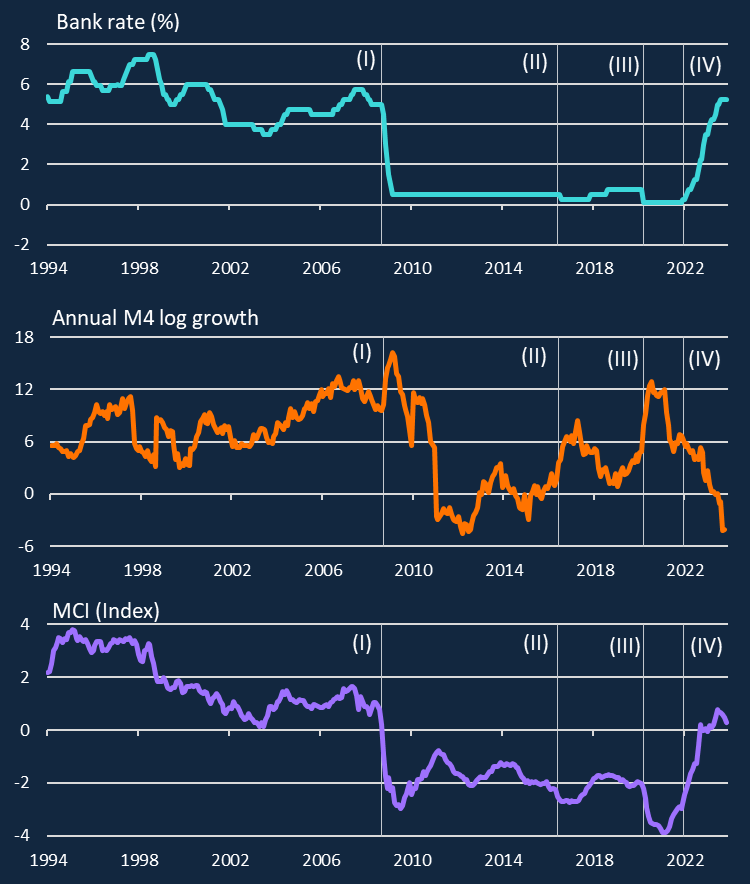

Chart 1 plots the UK MCI in the bottom panel and some key input variables that feed into it. To interpret the UK MCI, note that it is normalised by subtracting its mean and dividing by its sample standard deviation. As such, we place less weight on the level of the UK MCI, and more on changes. As Batini and Turnbull (2000) highlight, you cannot make a statement about degrees of tightness, but you can make relative statements, such as whether monetary conditions are tightening or easing.

Chart 1: UK MCI and selected input variables

Notes: The index is expressed in standard deviations from average. Stalks denote: (I) GFC; (II) EU Referendum; (III) Covid-19; and (IV) start of tightening cycle. Latest observation: November 2023.

Sources: Bank of England, Bloomberg Finance L.P, Tradeweb and Bank calculations.

Our index points to a loosening in UK monetary conditions during previous stimulus episodes. The UK MCI drops significantly during the GFC (Chart 1, Stalk I), consistent with the MPC’s conventional and unconventional monetary policy actions. The UK MCI also suggests monetary conditions eased as a result of monetary policy actions following the EU Referendum (Stalk II) and Covid-19 (Stalk III), however less so than during the GFC.

During the recent tightening cycle (Stalk IV), the UK MCI increased slightly earlier than Bank Rate, reflecting the slowing pace of QE purchases in 2021. The tightening over 2021–23 was driven first by reduced balance sheet flows, and then moves in the yield curve, first at the short end, and then also at the longer end. The UK MCI also suggests that monetary conditions have loosened slightly since peaking in September 2023.

It is important to keep in mind that the UK MCI presented here is a statistical construct and reflects only one approach to measuring monetary conditions. Our modelling strategy is designed to weight together variables based on their historic comovement with each other, not their correlation with GDP or inflation. Due to our use of fixed weights, any state-contingent effects of policies are only indirectly captured in our index, to the extent that it is reflected in interest rates. That said, to the extent that monetary conditions transmit changes in the monetary stance to the real economy, it is plausible that our UK MCI provides some information about future macroeconomic outturns. Preliminary analysis is consistent with this view, though further research is required to substantiate the relationship between monetary conditions and the macroeconomy.

Conclusion

The UK MCI presented in this post provides a comprehensive new measure of UK monetary conditions, which synthesises information about both conventional and unconventional policies. Crucially, our measure shows material variation in the post-GFC period, when Bank Rate was constrained by the ELB. Indeed, it highlights that unconventional policy tools supported significant loosening in UK monetary conditions in response to the GFC and subsequent stimulus episodes. Even at times when the ELB is not binding, including the recent tightening cycle, the UK MCI provides more information about the evolution of monetary conditions, faced by economic agents, than a sole focus on Bank Rate would suggest.

Given that unconventional tools are now an established part of the monetary toolkit, further research into monetary conditions, and what they imply for macroeconomic outcomes, remains important.

Natalie Burr and Julian Reynolds work in the Bank‘s External MPC Unit, and Mike Joyce works in the Bank’s Monetary and Financial Conditions Division.

If you want to get in touch, please email us at [email protected] or leave a comment below.

Comments will only appear once approved by a moderator, and are only published where a full name is supplied. Bank Underground is a blog for Bank of England staff to share views that challenge – or support – prevailing policy orthodoxies. The views expressed here are those of the authors, and are not necessarily those of the Bank of England, or its policy committees.

Share the post “To the lower bound and back: measuring UK monetary conditions”

Publisher: Source link

{kind=link}

{kind=link}

{kind=link}