Krishan Shah, Phil Bunn and Marko Melolinna

An important way in which monetary policy impacts the economy is through its effects on the capital expenditure of firms. When policy rates are raised (and as long as risk-premia remain unchanged) firms’ cost of capital increases. A higher cost of capital should lead firms to increase their required return (or hurdle rate) on investment, resulting in fewer projects exceeding the hurdle rate and less investment overall. For monetary policy to impact investment, changes in the cost of capital need to pass through to hurdle rates. Using new survey evidence, we find that hurdle rates for UK firms tend to be high, and they have responded sluggishly to higher interest rates over the past two years.

A recent literature uses a combination of survey data and information scraped from earnings calls to explore how (predominantly large, US-based) firms set hurdle rates. It finds that firms set hurdle rates far in excess of the cost of capital they face, that the size of this wedge between the hurdle rate at the cost of capital is positively related to idiosyncratic risk and market power, and that firms do not frequently change their hurdle rates. To understand if a broader set of UK firms use hurdle rates, and how they have responded to the recent large increase in interest rates, we asked firms in the Decision Maker Panel (DMP) whether they set investment hurdle rates and how the rates they have set have changed over time.

Hurdle rates are used by almost a third of firms

Across all 2,227 firms surveyed, approximately 30% reported that they set an investment hurdle rate. This proportion is approximately in line with the proportions of firms who used ‘mixed strategies’ (referring to firms using hurdle rates and relative rates of return methods) in the 2016 Finance and Investment Decision Survey which previously asked about this topic.

We also asked firms what alternative methods they use to make investment decisions if hurdle rates are not employed. The most popular response, provided by almost 40% of respondents not setting hurdle rates, was that they replace capital items at fixed intervals. This suggests firms not using hurdle rates tend to invest in a more ad-hoc manner. Around 20% of firms reported that they set a target payback period for investments.

Hurdle rates are used by larger and more leveraged firms who are more likely to invest

Looking across sectors (Chart 1) the use of hurdle rates is most common among firms operating in the real estate sector, with 45% of firms reporting that they set a hurdle rate, while around 37% of firms in the manufacturing and other production sectors do so. By contrast only 12% of firms in the other services sector and 20% in the professional and scientific services and information and communications reported using hurdle rates. This difference suggests that hurdle rates are more commonly used by firms making tangible investment. Larger firms are also more likely to use hurdle rates than smaller firms: over 40% of firms with 250+ employees use a hurdle rate compared to under 20% for those with 10–49 employees. Given that bigger firms account for a substantial proportion of aggregate business investment, a larger proportion of capital expenditure decisions will likely be tied to hurdle rates: weighting by reported investment raises proportion of firms using hurdle rates to 45%.

The use of hurdle rates is higher among firms that primarily use external finance rather than internal cash flow to fund investment. Firms who use hurdle rates also report reviewing their investments more frequently than those not using hurdle rates. This suggests that hurdle rates are employed by more sophisticated firms that regularly invest.

Chart 1: Proportion of firms reporting using investment hurdle rates by sector

Note: Based on question ‘Does your business set an investment hurdle rate, ie a target rate for the total rate of return required on investment expenditure?’.

Hurdle rates are high and have been sticky over recent years

Looking at the hurdle rates that firms use, and how they have changed over time, provides a view on how they may affect the transmission of monetary policy. In general, hurdle rates tend to be high relative to firms cost of capital (Chart 2). Hurdle rates have increased since the start of the recent tightening cycle at the end of 2021, but by less than the increase in policy rates and the interest rates paid on loans by companies – which also captures variations in risk premia (Chart 2). The mean hurdle rate is estimated to have increased from 14.7% in 2018 to 15.5% in 2021 and then to 16.4% in 2024. The median hurdle rate has similarly increased from 12% to 14% between 2018 and 2024, but remained unchanged between 2018 and 2021 at 12%. These values are close to averages in found in the wider literature (Jaganathan et al (2016) and Gormsen and Huber (2023)).

Chart 2: Mean and median reported hurdle rate over time and average official bank rate and average interest rate on loans to private non-financial corporations (PNFCs)

Notes: Based on question ‘Does your business set an investment hurdle rate, ie a target rate for the total rate of return required on investment expenditure?’. The reported values have been winsorised at the 5th and 95th percentiles.

One reason that hurdle rates may have risen more slowly than policy rates is that firms report adjusting their hurdle rates infrequently. Chart 3 shows that while 52% of firms reported having adjusted their hurdle rates during the last two years, 30% report having not changed their hurdle rates in over three years. Almost 60% of firms that report using external finance to fund their investment reported having adjusted their hurdle rates within the past two years.

Chart 3: Proportion of firms reporting when they last adjusted their hurdle rate

Note: Based on question ‘Approximately, when did your business last change the investment hurdle rate that it sets?’.

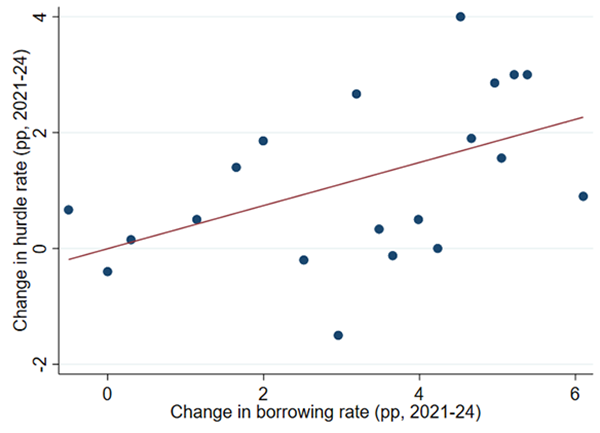

To see how changes in hurdle rates relate to the change in the cost of financing they face, in Chart 4 we focus on firms that use external finance to fund investment. We find a significant positive relationship between the change in firms’ reported borrowing costs since 2021 and the change in their reported hurdle rates over the same period. The slope suggests that a 1 percentage point increase in the borrowing rate these firms face is associated with a 0.37 percentage point rise in their hurdle rates. So, while the rise in policy rates have been associated with some increase in hurdle rates, the magnitude of change has been smaller than the change seen in borrowing costs. This is suggestive of a reduced feedthrough of changes to firms’ cost of capital to their required rate of return on investment, although we have not conducted a more formal identified analysis.

Chart 4: Change in reported borrowing rates and hurdle rates: firms using external finance to invest

Notes: Binned scatterplot based on question ‘What is the percentage investment hurdle rate that your business sets, both now and back in 2021?’ and ‘What is the approximate average annualised interest rate on the interest-bearing borrowing that your business has both now and at the end of 2021?’.

Sticky hurdle rates are associated with a smaller investment response to higher interest rates. We find that firms which have adjusted their hurdle rates within the last six months report substantially larger cuts to investment (of around 20%) as a result of higher interest rates, while firms that last adjusted their hurdle rates over three years ago reduced their investment by only 5% on average.

Conclusion

A significant minority of firms set an investment hurdle rate which they use to evaluate investment projects. The firms that set hurdle rates are larger, are more likely to use external finance for investment, and tend to evaluate their investment plans more regularly than those that do not. Hurdle rates tend to be higher than firms’ cost of capital. While both average borrowing rates and policy rates have increased markedly over the past three years, the average hurdle rate has only increased more modestly, by around 2 percentage points over this period. Firms do not frequently adjust their hurdle rates, and when they do these changes are smaller than the associated changes seen in firms cost of borrowing. The slow adjustment of hurdle rates could have implications for firms’ investment responses to monetary policy, suggesting a potentially slower pass-through of interest rate hikes to aggregate investment than often assumed in theory.

Krishan Shah, Phil Bunn and Marko Melolinna work in the Bank’s Structural Economics Division.

If you want to get in touch, please email us at [email protected] or leave a comment below.

Comments will only appear once approved by a moderator, and are only published where a full name is supplied. Bank Underground is a blog for Bank of England staff to share views that challenge – or support – prevailing policy orthodoxies. The views expressed here are those of the authors, and are not necessarily those of the Bank of England, or its policy committees.

Share the post “High hurdles: evidence on corporate investment hurdle rates in the UK”

Publisher: Source link

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}