Marco Garofalo, Giovanni Rosso and Roger Vicquery

Most international trade is denominated in dominant currencies such as the US dollar. What explains the adoption of dominant currency pricing and what are its macroeconomic implications? In a recent paper, we explore a rare instance of transition in aggregate export invoicing patterns. In the aftermath of the depreciation that followed the Brexit referendum in 2016, UK exporters progressively shifted to invoicing most of their exports in dollars, rather than in pounds. This was driven by firms more exposed to currency mismatches, eg exporting in pounds but importing in dollars before the depreciation. As a result of this aggregate transition to dollar pricing, a dollar appreciation now depresses demand for UK exports by twice as much than before 2016.

A dominant currency pricing transition

Recent studies on international invoicing find currency choice of exporters to be a remarkably persistent phenomenon at the aggregate level, for example in the cross-country data set on invoicing currencies compiled by Boz et al (2022). The stable and outsized role of the dollar in global trade invoicing has given rise to a Dominant Currency Paradigm (Gopinath et al (2020)) underpinned by network effects and strategic complementarities.

In stark contrast with the cross-country evidence is the story told by UK transaction-level data on exports and imports of goods recorded by His Majesty’s Revenues and Customs (HMRC). Until 2016, the majority of UK non-EU exports were invoiced in the ‘producer’ currency, the British pound. However, in the aftermath of the June 2016 Brexit referendum and the subsequent depreciation of the pound, the share of non-EU UK exports invoiced in pounds started to sharply decrease. It went from about 55% in 2015 to 35% in 2022. At the same time US dollar (USD) invoicing has surged from around one third to nearly 55% (Chart 1). Thus, the majority of extra-EU UK exports is now invoiced in the dominant currency of the international pricing system, the USD: a Dominant Currency Pricing Transition.

Chart 1: Invoicing shares of UK non-EU exports including (left side) and excluding (right side) the US

Source: HMRC administrative data sets, UK non-EU exports.

Invoicing currency choice and foreign-exchange mismatches

Why did this transition to dollar pricing materialise? We answer this question relying on transaction-level data on the universe of UK trade between 2010 and 2022. While invoicing choices are commonly thought as the result of network externalities (Amiti et al (2022)), these factors are unlikely to explain a rapid aggregate shift in currency pricing equilibria. Our paper highlights the role of currency mismatches in the face of a large FX shock in generating such a transition.

We begin by documenting firm-level currency mismatches in the UK in the wake of the Brexit depreciation. Prior to 2016, UK firms were pricing most of their exports in GBP while at the same time importing foreign inputs mostly invoiced in USD or other currencies. With prices sticky in the currency of invoicing, the sudden GBP depreciation reduced revenues and increased marginal costs for such firms. We define the firm-level net exposure to mismatches in a particular currency – say the pound – as the firm’s exports invoiced in GBP minus imports invoiced in GBP, normalised by the firm’s total gross trade. Chart 2 plots this measure of exposure on the horizontal axis against the post-2016 reduction in GBP invoicing on the vertical axis. The more firms had a ‘long’ operational exposure to the GBP, the more they reduced the share of their export receivables invoiced in GBP after 2016. This points to valuation effects from the Brexit referendum depreciation to have played a role in changing invoicing choice equilibria.

Chart 2: Firm-level currency mismatches and reduction in GBP invoicing

Source: HMRC administrative data sets, UK non-EU non-US exports, 2010–22.

Note: On the y-axis is plotted the firm-level change in GBP share of exports between 2015 and 2019 in percentage points. The x-axis plots bins of ‘exposure to GBP’, ie firms’ exports in GBP minus imports in GBP. Each bin is labelled with the corresponding level of exposure as a per cent of gross trade. The arrows as well as the density of bins on the right tail of the distribution indicate that many more firms are ‘long’ GBP than ’short’ or hedged.

We compute a firm-level measure of such valuation effects by combining our measure of currency-mismatch exposure by invoicing currency with firm-level effective exchange rates, composed of the bilateral depreciations of the GBP vis-a-vis each firm’s destinations currencies. This ‘currency-mismatch valuation shock’ can be easily interpreted as the potential gain or loss experienced by firms with currency mismatches, in percentage of their gross trade.

Chart 3 plots the average value of this measure in the cross section for each year in the sample. It is evident that in 2016 UK firms experienced an unprecedented foreign-exchange mismatch valuation shock , with an average loss in absence of price adjustment or financial hedging of 4% of gross trade.

Chart 3: Currency-mismatch valuation effects

Source: HMRC administrative data sets, UK non-EU non-US exports, 2010–22.

Note: The graph plots currency-mismatch valuation effects, averaged across firms, ie the average potential gain/loss from GBP exchange rate movements experienced on average in the sticky prices limit. Negative values represent losses.

In our paper, we uncover the causal effect of a FX mismatch valuation shock on invoicing relying on both shift-share and event-study empirical designs.

In our shift-share exercise, the share of exports invoiced in a given currency are regressed on our valuation effect measure – holding mismatch exposure fixed at the pre-referendum level to ensure our results can be given a causal interpretation – as well as on proxies for the traditional drivers of invoicing currency decisions such as strategic complementarities and market power. The latter matter because if exporters are targeting the price of their closest or largest competitors, then choosing the same currency as them makes the task easier. On the other hand, if seller and buyer have conflicting optimal currency choices, the respective market power can decide in which direction the equilibrium outcome will swing. We find that foreign-exchange valuation shocks matter for invoicing decisions above and beyond these more classical channels. Our results imply that for a firm exposed 100% of its gross trade to the GBP, a GBP depreciation of 1% is expected to drive a reduction in GBP invoicing by 1 percentage point, together with a shift towards USD invoicing by a similar amount.

Turning to our event-study specification, we investigate the dynamic effects of the Brexit currency-mismatch valuation shock on invoicing decisions at the firm-product destination level and monthly frequency. Chart 4 highlights the results of this event-study, depicting leads and lags of a coefficient capturing the differential reduction in GBP invoicing for firms experiencing bigger valuation shocks around the Brexit referendum. The majority of the response to the currency-mismatch channel occurs in the first year since the Brexit referendum depreciation, and then assumes a more gradual pace over latter of the sample. Importantly though, its impact appears to be persistent and monotonically dragging on GBP invoicing shares.

Chart 4: The dynamic effect of currency-mismatch valuation effects on GBP invoicing

Source: HMRC administrative data sets, UK non-EU exports and imports, 2010–22.

Note: The graph plots the leads and lags of the coefficient for currency-mismatch valuation shock from the dynamic specification in Equation 3 of our paper, capturing the differential reduction in GBP invoicing for firms with high exposure to foreign-exchange mismatch valuation effects.

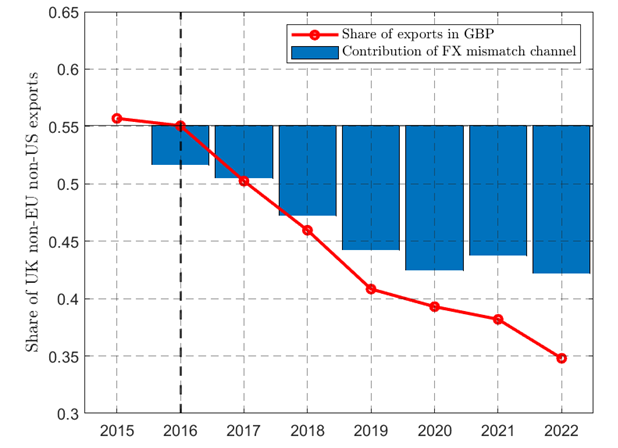

Chart 5 shows the results of a simple quantitative exercise assessing the relevance of this channel. The currency-mismatch valuation channel appears to be able to explain most of the swift decline of the pound as an invoicing currency observed since 2016.

Chart 5: Contribution to aggregate shift in GBP from the currency-mismatch valuation channel

Source: HMRC administrative data sets, UK non-EU exports, 2010–22.

Note: The red line is the aggregate share of exports invoiced in GBP as in Chart 1. The blue bars show how much of the dynamics of the red line can be explained by the foreign-exchange mismatch valuation channel.

Macroeconomic implications: UK trade is now twice as sensitive to USD movements

We find that this dramatic transition to dollar pricing had meaningful macroeconomic consequences, with important implications for the way international spillovers are absorbed by the UK economy. In particular, UK exports are now significantly more sensitive to movements in the dollar.

We show this employing two econometric strategies. First, we exploit differential exposure of firms to different destination currencies and the granularity thereof (ie the fact that only few destinations account for a large share of a firm’s exports). We construct firm-level ‘granular’ effective exchange rates by aggregating the idiosyncratic components of destination-USD exchange rates, weighted by the export share of that destination for the firm. We then use this measure in a micro-to-macro local projection regressions (Jordà (2005)) to estimate the aggregate response of export values to exchange rate movements. We observe that while export values of non-USD exporters hardly respond to USD exchange rate movements, USD exporters have a negative, significant and persistent response (Chart 6, left side). This establishes at the granular level that USD invoicers respond more to USD movements than non-USD invoicers.

Second, we ask: has the micro elasticity of quantities to exchange rate movements changed? In order to test this hypothesis, we employ a second econometric specification in the spirit of the work by Amiti et al (2022). It is a two-stage procedure, where a regression of export prices in foreign currency onto exchange rates represents the first stage, while a regression of quantities on (fitted) prices is the second stage. In both stages, we control for high-dimensional firm, destination-product and time fixed effects.

Chart 6: Dynamic response of export value to an effective firm-level USD exchange rate appreciation

Source: HMRC administrative data sets, UK non-EU exports, 2010–19.

Note: The two lines represent the response of UK export values to movements in the granular firm-level USD effective exchange rate. On the left-hand side we compare USD versus non-USD invoicers throughout the sample. On the right-hand side we compare the aggregate impact on all firms before and after 2016. Shaded areas are 95% confidence intervals.

We find that the elasticity of export quantities to USD exchange rate movements doubled from the pre-2016 to the post-2016 period, both in the short and medium run. In both periods, as intuition would suggest, an appreciation of the USD vis-a-vis the domestic currency of the customer causes a fall in demand and thus in export quantities (Chart 6, right side).

Conclusion

We explore a unique episode of transition to dominant currency pricing and show that, in the presence of operational currency mismatches, a large, unexpected shock to the level of the exchange rate can generate a rapid aggregate change in invoicing patterns. This highlights the fact that dominant currency equilibria are not immutable, despite the pervasiveness of network effects in the international monetary system documented in the recent literature, with important implications for the debate on the outlook of global dollar dominance.

The dollarisation of UK trade also has first-order macroeconomic implications. Compared to the pre-Brexit referendum period, demand for UK exports is now twice more sensitive to USD exchange rate movements. This could have important consequences for monetary policy, as higher dollar sensitivity might affect the foreign-exchange transmission channel and alter normative considerations on the optimal conduct of policy.

Marco Garofalo and Roger Vicquery work in the Bank’s Global Analysis Division. Giovanni Rosso is a PhD Economics student at University of Oxford.

If you want to get in touch, please email us at [email protected] or leave a comment below.

Comments will only appear once approved by a moderator, and are only published where a full name is supplied. Bank Underground is a blog for Bank of England staff to share views that challenge – or support – prevailing policy orthodoxies. The views expressed here are those of the authors, and are not necessarily those of the Bank of England, or its policy committees.

Share the post “Selling England (no longer) by the pound: currency-mismatches and the dollarisation of UK exports”

Publisher: Source link

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}