Michael Kumhof and Mauricio Salgado-Moreno

While ‘unconventional’ balance-sheet policies like quantitative easing (QE) and quantitative tightening (QT) appear to have been successful, it is difficult to separate their macroeconomic and financial stability implications from those of other polices. Hence, in a recent paper, we develop a theoretical framework, focusing on the central bank’s liabilities, that sheds light on these implications. The key model feature is the inclusion of a detailed financial system with both heterogeneous banks and non-bank financial institutions that allows us to identify the transmission of QE/QT policies. Our framework provides guidance to policymakers interested in using new combinations of balance sheet and interest rate policies by highlighting the relevance of the interbank market and financial frictions in the transmission of balance sheet policies.

The bulk of existing theoretical work on QE/QT focuses its attention on the asset side of the central bank balance sheet, specifically the effect of asset purchases on interest rates and real activity. Instead, our paper focuses more on the liability side, specifically the effect of reserve issuance, reserve distribution across banks, and policy rules for reserves, on both steady state allocations and financial and real stability in response to shocks. To help us do so, we draw from recent empirical studies across advanced economies.

What we do

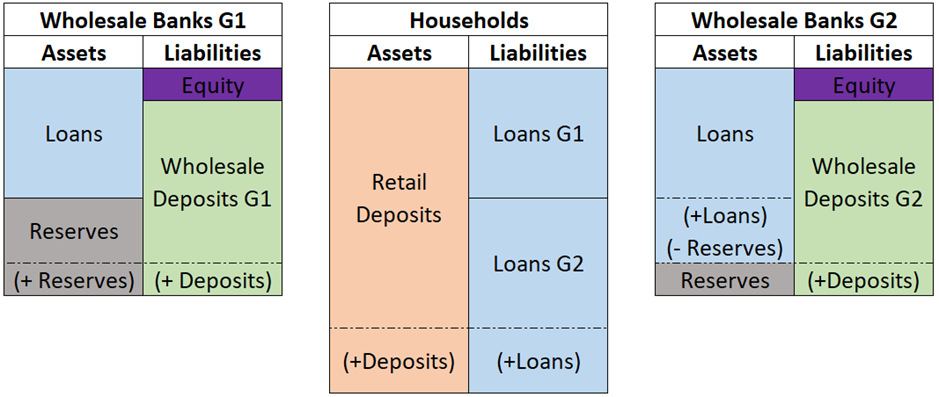

We develop a medium-scale New-Keynesian DSGE model with a fully specified real sector and a detailed financial sector calibrated to the post-GFC pre-Covid US economy. Figure 1 provides an overview of the model’s financial sector. In addition to the standard set of agents in the type of medium-scale model that is commonly used by central banks, the model also contains two ex-ante heterogeneous groups of commercial banks, relatively reserve-scarce (B2) and relatively reserve-abundant (B1) banks, that make household loans, compete to retain household deposits, settle net deposit withdrawals in reserves, and lend/borrow reserves in an interbank market.

Figure 1: Overview of the model’s financial sector

Our aim is to study interbank markets that link solvent banks with different liquidity levels. Thus, our reserve-scarce banks capture financially sound institutions that are only in relative terms less liquid than our reserve-abundant banks. This provides the necessary environment for an interbank market to exist, while allowing us to remain agnostic on the reasons behind a given liquidity distribution. In practice this distribution will be determined by several factors, not included in our model, like market power, business models, household preferences, etc. The Bank of England considers UK banks to have appropriate levels of capital and liquidity which should ensure that QT will not induce interest rate volatility on its way to its steady-state balance sheet size.

We model QT (QE) policies via central bank sales (purchases) of bonds to (from) non-bank financial institutions (NBFIs), which is close to how central banks have implemented such policies. Figure 2 depicts the central bank’s balance sheet changes during QT. The central bank sells assets, principally government securities, to NBFIs. NBFIs’ payment to acquire these assets reduces their wholesale deposits (retail deposits are only affected indirectly), while commercial banks settle these payment instruments with the central bank via a reduction of their reserve holdings (recall that only banks can hold reserves). As a result, commercial banks’ balance sheets contract.

Figure 2: Quantitative tightening flowchart

Our model reflects the reality that banks do not face financing risks, only refinancing risks. In other words, banks always finance new loans by creating new deposits, so that there is never a risk of not being able to finance a new loan. But there is a risk of having to refinance lost deposits, that means, banks are subject to the risk of being unable to settle net deposit withdrawals in reserves.

Such net deposit withdrawals allow us to capture, in a reduced-form way illustrated in Figure 3, modern bank runs, where institutional investors (MMFs in our model), rather than retail depositors, disproportionately flee from less liquid (B2 banks) to large liquidity-rich (B1) banks, similar to the US experience in March 2023.

Figure 3: Net deposit withdrawals flowchart

We study the effects of QE/QT from two complementary perspectives. First, we study the comparative static effects of the aggregate quantity of reserves and government debt on steady state interest rates and macroeconomic variables. Second, we study the dynamic effects of policy surprises that propagate through the banking system to real macroeconomic variables.

What we find

For the comparative static analysis, we find that reductions in the quantity of reserves (QT) trigger an increase in interbank borrowing, at higher interbank and wholesale deposit interest rates, by reserve scarce (B2) banks. Figure 4 shows these baseline results. For the policy rate there are two offsetting effects of QT. First, because the central bank reduces the stock of aggregate reserves by selling some government debt back to private bond investors, the interest rate risk premium on government debt that these investors demand rises. Second, at significantly lower levels of reserves a growing liquidity scarcity makes the remaining reserves more valuable and therefore reduces the interest rate that the central bank needs to pay. For sufficiently large QT, the second effect dominates and the equilibrium real policy (reserves) rate falls.

Figure 4: Steady-state effects of QT (and QE)

Key model variables’ steady state as a function of central bank’s supply of reserves. All horizonal axes show the total reserves to GDP ratio (in %). In each subplot, the intersection of the black vertical line and the orange horizonal line depict the initial (calibrated) steady state, while the blue curves represent the steady state of each variable at different levels of reserves. To the left of the black vertical line the model’s economy experiences permanent QT, while to the right of the black vertical line we see the steady state implications of permanent QE policies.

Key financial and real variables deteriorate due to an increase in the cost at which especially the reserves-scarce parts of the banking sector can create money. In the paper we provide further information on the optimality conditions for all agents in the model, but here it suffices to say that the demand for reserves is determined primarily by the presence of reserve scarcity costs that capture the convenience from holding liquid assets as a function of each bank’s level of deposits relative to reserves. Because the quantity of loans declines and the opportunity cost of holding deposit money increases as reserves become scarcer, GDP drops by around a third of a percentage point for a permanent halving of the quantity of reserves.

Moving beyond QT and steady states, we find that large-scale net deposit withdrawal shocks from reserve-scarce (B2) to reserve-abundant (B1) banks have highly asymmetric effects, with very small effects on reserve-abundant banks but very large effects on reserve-scarce banks that trigger much higher lending rates and thus cost of money creation in that part of the banking system, and as a result potentially sizeable declines in GDP (Figure 5).

Figure 5: Dynamic responses to a net deposit withdrawal shock

Key model variables’ impulse responses to a net deposit withdrawal shock that shifts liquidity from B2 to B1 banks. Black lines depict aggregate variables, while green and red lines show the responses for relatively reserve-abundant B1 banks and relatively reserve scarce B2 banks, respectively. Horizonal axis in quarters with shock at period zero.

In the paper we show that if the central bank responds to a widening of interbank rate spreads by injecting additional reserves, it can significantly reduce the contractionary effects of this type of shock. We find that the quantity and distribution of central bank reserves, and the extent of frictions in the reserves and interbank markets, critically affect the size of these effects, and can matter even in a regime of ample aggregate reserves.

By contrast, large-scale lending booms have almost no effects on reserve scarcity if they are symmetric across banks, due to netting of deposit inflows and outflows, and moderate effects if they are asymmetric, as illustrated in Figure 6. The reason for the moderate effects is that the aggressive group of banks that creates deposits out of lockstep with other banks will lose some, but not all, of its newly created deposits. Therefore, the aggressive lenders will also lose some reserves to other banks. Such shocks are expansionary at the aggregate level because the loss of reserves experienced by the aggressive lenders merely dampens but does not fully offset the increase in their willingness to create money.

Figure 6: Asymmetric lending boom flowchart

Finally, we study the optimal set of responses for a central bank that has both conventional interest rate and ‘unconventional’ balance sheet tools at its disposal. To answer this, in the paper, we perform a more technical welfare analysis of different combinations of Taylor rules for the interest rate on reserves, with a response to inflation, and reserve quantity rules, with a response to the interbank lending spread. We find that if deposit withdrawal shocks are empirically important, aggressively countercyclical reserve quantity rules can make a sizeable contribution to welfare, even on a par with an aggressively countercyclical Taylor rule.

Key takeaways

Our theoretical framework provides several insights concerning the macroeconomic and financial stability implications of QE/QT and of aggregate and sectoral reserve shortages. First, the distribution of reserves across the banking system is an important determinant of the effects of QE/QT policies, which are highly asymmetric for reserves-scarce banks. Second, countercyclical reserve injections during periods of interbank market stress have beneficial output as well as financial effects. The same is true for policies that reduce frictions in the reserves and interbank markets. Such frictions include business costs of temporary reserve shortages and informational frictions in interbank lending. Finally, the effects of QE and QT on the equilibrium policy rate show a trade-off between a higher liquidity scarcity interest rate discount at low levels of reserves and a lower government debt interest rate risk premium at high levels of reserves that reduce outstanding government debt.

Central banks now have an additional balance sheet tool that can be used for financial and real stabilisation purposes. In reality this new tool can take several forms such as short-term repo facilities or ad-hoc purchase programmes. Nevertheless, further work remains to be done to better understand the interactions between conventional monetary policy via interest rates and the optimal size, and composition, of the balance sheet of central banks. We believe that our model provides a useful starting point to analyse these and other related questions.

Michael Kumhof works in the Bank’s in the Bank’s Research Hub and Mauricio Salgado-Moreno works in the Bank’s Monetary and Financial Conditions Division.

If you want to get in touch, please email us at [email protected] or leave a comment below.

Comments will only appear once approved by a moderator, and are only published where a full name is supplied. Bank Underground is a blog for Bank of England staff to share views that challenge – or support – prevailing policy orthodoxies. The views expressed here are those of the authors, and are not necessarily those of the Bank of England, or its policy committees.

Share the post “Central bank balance sheet policies and the market for reserves”

Publisher: Source link

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}