David Glanville and Arif Merali

Short term interest rate (STIR) futures are the bedrock of interest rate markets, used to price expectations of central bank policy rates and other UK rate derivative markets such as swaps and options (see Figure 1). They are key for the transmission of monetary policy and provide an avenue for interest rate risk hedging which is important for financial stability. Financial market liquidity usually worsens when volatility rises, however liquidity in the UK’s STIR futures during 2022 was especially poor. Liquidity in some metrics such as open interest and volumes has since improved as volatility has reduced, however our extensive market intelligence conversations suggest that many still believe there is further to go when looking ‘under-the-bonnet’ at another key metric, market depth. Volatility continues to play a role, but a reversion to publishing key data releases within market hours may help to build liquidity further.

Figure 1: SONIA futures underpin liquidity across a range of sterling derivatives

What are SONIA futures?

SONIA (Sterling Overnight Index Average) is the risk-free interest rate benchmark in the UK, and markets transitioned to SONIA from the tainted sterling LIBOR index at the end of 2021. SONIA futures are a subset of STIR derivatives contracts used by market participants to manage interest rate risk or speculate on moves in SONIA, which tracks Bank Rate closely. They are the foundation of a much wider set of interest rate derivatives both in terms of pricing and liquidity, such as interest rate swaps used by banks and building societies as references for fixed-term mortgages. Banks and building societies offset or ‘hedge’ their mortgage exposures in the swaps market via market-makers, who themselves often hedge their resulting interest rate risk in the SONIA futures market. If SONIA futures are illiquid, it’s more difficult and expensive for market-makers to hedge risk, and means these demand/supply imbalances can distort the swap market – potentially making new mortgages more expensive.

SONIA futures and monetary policy

Because of their importance for the pricing of interest rate swaps and mortgage rates, SONIA futures are highly influential on the transmission for monetary policy as well as for the reliability of signals taken by policy makers from market pricing.

A deep and liquid SONIA futures market ensures that forward-looking market pricing for Bank Rate reflects a more realistic assessment of market participants’ mean expectations of the likely future policy setting. The ‘Mini-Budget’ at the end of 2022 and the 2020 ‘dash-for-cash’ episodes are two examples of when the SONIA futures market dislocated materially from what market participants saw as an appropriate reflection of fundamentals. According to the Bank’s Market Participants Survey (MaPS) results during the ‘Mini-Budget’ for example, market participants ascribed a third of the divergence between market pricing and Bank Rate expectations to ‘market illiquidity and technical factors’.

SONIA futures and financial stability

Interest rate derivatives including SONIA futures are used extensively by both banks and non-bank financial institutions to hedge interest rate risk, and when liquid, enable the efficient transfer of that risk across the financial system, thereby aiding financial stability. Derivatives markets are heavily interconnected with each other and other core UK markets such as the gilt market, which can further amplify shocks in the financial system.

Additionally, the primary liquidity providers in the SONIA futures market are algorithmic traders. Although algorithms support market liquidity in ‘normal’ times, generating high volumes very quickly, their propensity to ‘turn off’ during risk events can drain liquidity rapidly during periods of volatility as they have no obligation to provide prices.

Liquidity in SONIA futures

At the start of the hiking cycle at the end of 2021, which coincided with the timing of the risk-free rate transition to SONIA, liquidity across a range of metrics (market depth, open interest, and volumes) notably worsened, and this continued into 2022 (see Charts 1, 2 and 3). Some suggested this was due to the transition itself, however most market participants determined that the decline was primarily a result of the substantial increase in interest rate uncertainty and volatility as central banks globally readjusted monetary policy settings to tackle inflation. Russia’s invasion of Ukraine and the ‘Mini Budget’ in 2022 also contributed to excessive market volatility.

Chart 1: Sterling STIR futures average top of book market depth by contract group

Sources: BMLL and Bank calculations.

Chart 2: LIBOR and SONIA Open Interest

Source: Bloomberg.

Chart 3: LIBOR and SONIA Volume (Rolling 30-day average)

Source: Bloomberg.

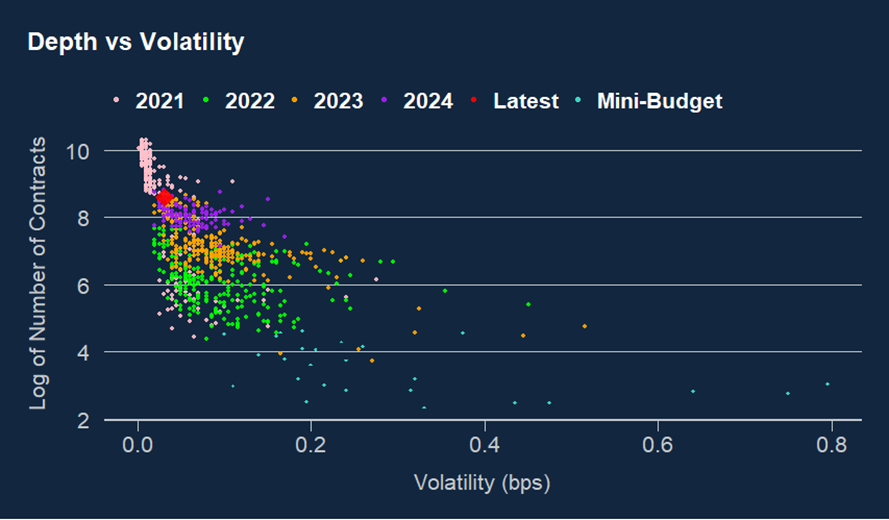

Of course, as volatility and uncertainty rise to extreme levels, market liquidity is expected to fall (see Chart 4). But according to conversations with market participants, UK STIR markets suffered to a greater extent than other jurisdictions (see Chart 5). Comparatively, when the US STIR futures market underwent a similar risk-free rate transition, it did not lead to a material reduction in liquidity. Given that UK market participants also do not tend to blame the UK’s risk-free rate transition as the cause of the initial decline in liquidity or the ongoing poor market depth, there are likely to be other UK-specific factors that were, and perhaps still are, at play.

Chart 4: The relationship between market depth and volatility

Sources: BMLL and Bank calculations.

Chart 5: STIR futures open interest across jurisdictions (indexed to 100)

Source: Bloomberg.

Under the bonnet illiquidity

Headline measures of SONIA futures liquidity such as open interest and volumes have improved markedly since 2022 (see Chart 2 and 3). Indeed, open interest and volumes are now broadly comparable to the old LIBOR days (adjusting for differences in LIBOR vs SONIA contract sizes), with volumes reaching record levels recently, supported by the prevalence of algorithmic traders.

Another liquidity metric known as price impact also shows a normalisation from the periods of stress in recent years as volatility has fallen from its extreme levels (see Chart 6).

Chart 6: The impact of trades on prices spikes in stress

Source: BMLL.

Even market depth when adjusted for the prevailing levels of volatility has improved each year since 2022 (see Chart 7). There is therefore no doubt that liquidity in many respects has improved materially. This is largely due to relatively less uncertainty over the future path of policy rates, as well as the extreme volatility experienced in 2022 now increasingly seen as in the ‘rear-view mirror’. A slowly increasing number of market-makers due to exchange incentives in the SONIA options market have also aided SONIA futures liquidity via the related hedging activity between those markets. That said, despite the improvements, market depth remains materially lower versus pre-hiking cycle levels. It also frequently hits very low levels during risk events, giving the SONIA futures market an ongoing sense of fragility compared to other markets, suggesting there is still diminished market participation outside of the algorithmic traders.

Chart 7: STIR futures market depth versus volatility for different time periods

Sources: BMLL and Bank calculations.

Liquidity begets liquidity

Stress events may still be weighing on appetites for UK risk exposure. The transition from LIBOR to SONIA futures meant a loss of a credit risk element that previously attracted basis-trading activity, although this is also true in the US.

But as highlighted, sentiment in recent months around the SONIA futures market has notably improved, reflected across a suite of liquidity metrics. And whilst volatility remains in check, it’s likely that liquidity will continue its upward trend as confidence and participation in the market improves – liquidity begets liquidity. However there is one notable element regarding the UK market specifically that could still be weighing on further improvements.

The topic of SONIA futures fragility continues to be frequently raised by market participants, particularly in the context of large moves in implied rates at times throughout the hiking cycle. One question we often get asked by market contacts is whether critical UK data releases such as CPI and labour market statistics, which are paramount to informing expectations about the future path of Bank Rate, will revert to being released during market trading hours. Prior to Covid, key data releases were at 09:30am, well within the SONIA futures market opening times. This meant the data hit the market when liquidity had already ‘woken up’ from the market open. However, with the current set up of the data releases being at 07:00am (originally moved because Covid made secure press briefings no longer possible, subsequently made permanent) some suggest the market open sees exacerbated price ‘gaps’, with algorithmic market-makers ‘switching off’, and the traditional bank market-makers simultaneously missing out on the surge in volumes they might experience during the usual price discovery process around such events. This is not the case across other jurisdictions such as the US and EA, which both have critical data releases within trading hours. Some market participants suggest that this factor continues to affect participation and hence liquidity, with market-making in UK derivative markets potentially less attractive versus other international markets, and end-users unable to efficiently hedge their risk in reaction to key data releases whilst the market is closed.

It is in everyone’s interest that UK short-term interest rate markets are as deep and liquid as they can be to ensure efficient monetary policy transmission and financial stability, and lots of progress has been made in this regard as the extreme volatility as decreased. The key question however is whether there is anything more that can be done to speed up further improvements and encourage greater participation. Changing data release times may not be a ‘silver bullet’ however. Some in the market may even prefer to have longer to think about what the data means for the likely path of policy, and there is perhaps some public benefit in data releases hitting the morning news headlines earlier. But it is at least a question worth considering if a reversion to the pre-Covid norm could encourage a healthier eco-system of participants in the SONIA futures market and other related markets.

David Glanville works in the Bank’s Sterling Markets Division and Arif Merali is a Senior Advisor across the Markets Directorate.

With thanks to Joel Mundy for data and analytics who works in the Bank’s Market Intelligence and Analysis Division.

If you want to get in touch, please email us at [email protected] or leave a comment below.

Comments will only appear once approved by a moderator, and are only published where a full name is supplied. Bank Underground is a blog for Bank of England staff to share views that challenge – or support – prevailing policy orthodoxies. The views expressed here are those of the authors, and are not necessarily those of the Bank of England, or its policy committees.

Share the post “Caring for the ‘future’”

Publisher: Source link

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}