Adam Brinley Codd, Daniel Krause, Pierre Ortlieb and Alex Briers

We both drive cars, but the US drives on the right while the UK drives on the left. We both walk, but we do so on sidewalks in the US and pavements in the UK. We both have asset managers, who want to take leveraged positions in interest rates. US asset managers had around US$650 billion of long treasury futures in June 2023. UK asset managers, in Autumn 2022, held around £200 billion in leveraged repo. However, the ways in which the financial system found willing lenders for these borrowers, and intermediated the risk through the system of market-based finance, differ.

This post explores the similarities and differences between the activity of asset managers and hedge funds in US Treasury (UST) futures markets, and the relationship between liability-driven investment (LDI) funds and lenders in the gilt repo market.

Why and how do asset managers use leverage?

Using leverage in an investment strategy involves borrowing (financial leverage) or derivatives (synthetic leverage) to gain higher exposure to risk factors and enhance returns. In order to offer higher returns to their investors, asset managers have, in principle, an incentive to use leverage. In practice, asset managers in the US and UK use leverage in different ways.

In the UK, many defined benefit pension schemes have long-term liabilities on account of the future payments they owe to their pensioners. Many pension schemes use LDI strategies (generally provided by asset managers) to match the profile of their assets to that of their liabilities and hedge their exposure to long-term interest rates and inflation. The basic building block of LDI strategies is long-term, index-linked government bonds. In leveraged LDI strategies, these bonds are used as collateral to borrow cash via repurchase agreements (repo) (see Figure 1, left panel). The cash received from these transactions is then invested in more long-term government bonds, increasing schemes’ sensitivity to (long-term) interest rates, and better matching their liabilities. An alternative but less common way for LDI funds to apply (synthetic) leverage is to use long-term interest rate swaps to receive a fixed rate while paying a floating rate. These leveraged LDI strategies allow pension schemes to increase their exposure to long-term gilts, while also holding riskier and higher-yielding assets, such as equities, in order to boost their returns and close potential funding gaps.

While US asset managers apply leverage for several reasons, boosting returns to outperform their benchmarks is a central motive. Leverage allows them to manage their portfolio duration and, at the same time, retain funds to invest in higher return assets, such as higher yielding corporate bonds, with shorter duration. One way asset managers achieve this in the US is by buying UST futures (see Figure 1, right panel). These contracts give asset managers exposure to a US Treasury bond, but without needing to pay for the whole thing up front.

How do markets find a lender for every borrower?

In the UK, LDI funds’ demand for leveraged gilt repo is intermediated by dealer banks. LDI funds borrow from dealer banks using term repo transactions with maturities of up to several months (see Figure 1, left panel). In using short-term repo funding to invest in long-term assets, LDI funds engage in maturity transformation. On the other side of the UK repo market, money market funds (MMFs) are an important provider of liquidity: they usually lend to dealers via overnight (reverse) repo. This is consistent with their mandates to invest in short-term safe assets which can easily be transformed into cash and transferred back to investors.

In the US, on the other hand, asset managers’ demand for leverage through US Treasury futures is mirrored by hedge funds’ net short positions (see right panel of Figure 1). However, for hedge funds, the short positions in UST futures are only one leg of a trading strategy known as the UST basis trade, which exploits an arbitrage opportunity from relatively higher UST futures prices compared to the underlying UST bonds. Hedge funds complete the UST basis trade by buying a cash bond that is eligible for delivery into the UST future and offsets their short position in the future. As the margins of this trading strategy are small, hedge funds try to increase their profits by using leverage. Like LDI funds in the UK, they borrow from dealer banks and MMFs in the repo market, using their UST bonds as collateral, to sell more UST futures and buy more UST bonds to hedge them. By doing so, hedge funds establish a link between asset managers’ demand for synthetic duration on one side and the US Treasury’s supply of longer-term bonds, helping to align prices in both markets. Their demand for repo funding also serves as a safe, short-term investment for MMFs and banks.

Figure 1: LDI and UST basis trade stylised intermediation chains

Sources: SMMD, Crane, SEC Private Fund Statistic and CFTC data, and Bank calculations.

How can leverage threaten financial stability?

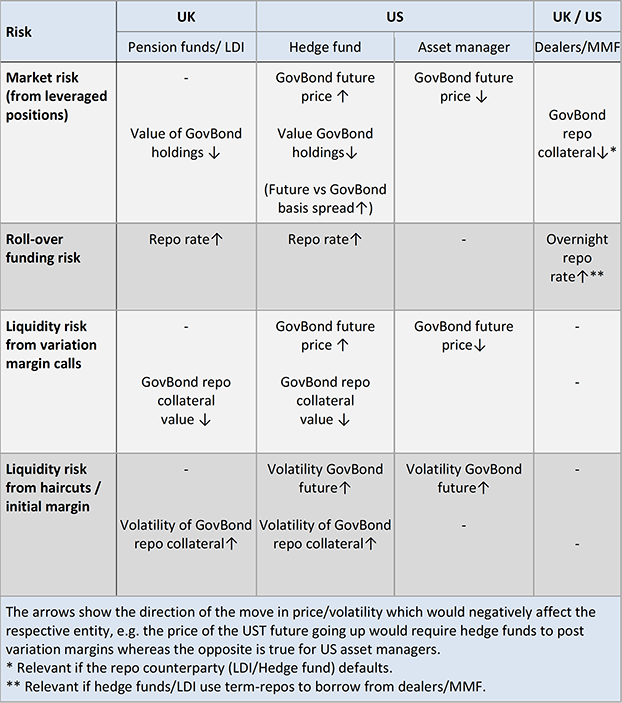

When it is not properly managed, leverage can jeopardise financial stability in a number of ways. A first channel has to do with prices. Leverage not only enhances returns but also amplifies losses when prices move in the wrong direction: in itself, this creates potential risks to counterparties as leverage makes defaults more likely. Furthermore, leveraged trades might become unprofitable if the cost of financing them increases (in Table A below, rows 1 and 2 describe how this risk is relevant for the respective entities in the intermediation chains described above). To prevent further losses, asset managers might decide to deleverage by closing their positions. Should they do so, the entire intermediation chain unwinds.

A second channel for potential risks from leverage has to do with collateralisation, which is a feature of both repo and derivatives markets. Counterparties to these transactions are required to post additional collateral whenever their derivatives positions, or the existing collateral posted in repo transactions, declines in value (eg variation margin). The same usually applies when volatility increases (eg initial margin and haircuts). Not having enough collateral at hand to meet this requirement when it arises could result in deleveraging (see Table A, rows 3 and 4).

An example is the severe and sudden repricing of the UK gilt market in Autumn 2022. Many LDI funds could not provide the additional collateral required on their repo and derivatives positions, and were forced to deleverage by selling long-term gilts into already stressed markets. This started a vicious spiral of falling gilt prices, collateral calls, and forced gilt sales which threatened financial stability. The Bank of England intervened via a temporary and targeted programme of purchases of long-dated gilts to restore market functioning. This gave LDI funds time to build their resilience to future volatility in the gilt market.

During the ‘dash for cash‘ episode in March 2020, many investors sold government bonds to raise cash, causing Treasury market illiquidity and putting severe strain on basis trading hedge funds. The spike in volatility caused by the onset of the Covid-19 pandemic increased the amount of collateral hedge funds had to post for their futures positions. Facing higher collateral requirements, mark-to-market losses, and higher refinancing costs in the repo market, hedge funds were forced to unwind parts of their basis trade positions. Therefore, hedge funds bought UST futures and sold the underlying bonds, widening the spread between futures and bond prices and exacerbating losses further. An intervention by the Federal Reserve prevented further spillovers to the US Treasury market that could have jeopardised financial stability.

Table A: Risks faced by the different entities in the intermediation chain

What does this comparison teach us about financial stability?

LDI strategies and the UST basis trade both represent an intermediation chain that link asset managers’ demand for leveraged long-term interest rate exposure on one side to a demand for short-term safe assets by investors such as MMFs on the other side, with dealer banks sitting between them. In that sense, both trades perform an important function for the financial system. But on both sides of the Atlantic this intermediation involves the use of leverage, which, if not properly managed, can threaten financial stability. However, there are clear differences between the two strategies; understanding and addressing risks in market-based finance therefore always requires a holistic and context-dependent approach to relevant markets, participants, and their interactions.

Adam Brinley Codd, Daniel Krause and Pierre Ortlieb work in the Bank’s Market-Based Finance Division. This post was written while Alex Briers was working in the Bank’s Market-Based Finance Division.

If you want to get in touch, please email us at [email protected] or leave a comment below.

Comments will only appear once approved by a moderator, and are only published where a full name is supplied. Bank Underground is a blog for Bank of England staff to share views that challenge – or support – prevailing policy orthodoxies. The views expressed here are those of the authors, and are not necessarily those of the Bank of England, or its policy committees.

Share the post “Leverage finds a way: a comparison of US Treasury basis trading and the LDI event”

Publisher: Source link

{kind=link}

{kind=link}

{kind=link}