Research Properties, Location and Price

When embarking on the journey to homeownership, thorough research into properties, locations, and prices is essential for making informed decisions.

Firstly, when browsing properties, ensure they fall within your price range, factoring in the maximum amount you can borrow along with your deposit.

Regarding the location, lenders typically consider an hour-long commute acceptable, but they may also take into account the possibility of remote work arrangements.

Do you consider living in a different county? Opting for a home in a nearby area could offer financial benefits, especially if you have the flexibility to work from home. Alternatively, opting for a property outside the city can result in substantial savings.

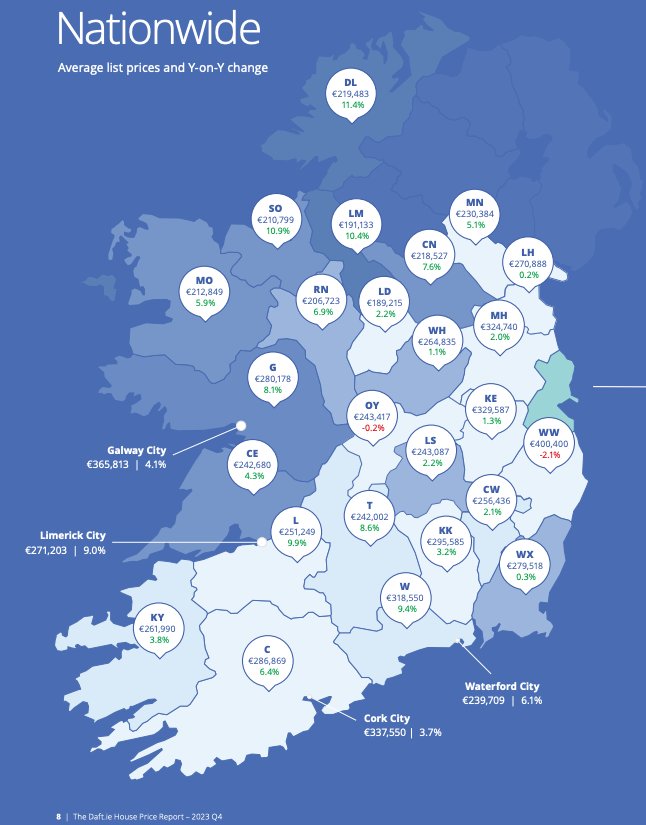

For instance, instead of choosing Galway City, where the average property price was €365,813 in Q4 2023, according to the Daft report, consider Galway County, where the average price was €280,723 during the same period. This decision could potentially save you €86,000.

By conducting thorough research and considering various factors, you can make a well-informed choice when purchasing your new home.

Read the Daft.ie House Price Report Q4 2023 here.

Manage Debt

Managing your debts effectively involves consistently making on-time payments, reducing outstanding balances, and keeping your debt-to-income ratio within acceptable limits.

Lenders assess not just your debt load but also your overall financial health and cash flow management.

You must meet the Central Bank of Ireland net disposable guidelines after all debt repayments.

If you can show that you’re comfortably meeting your existing debt obligations and still have significant leeway in your budget, it reassures lenders that adding a mortgage won’t pose a significant risk.

Establish a Good Credit History

Your credit history is really important when it comes to getting a mortgage. It shows how you’ve managed borrowing and repaying money in the past.

Lenders check your credit report to decide if they want to give you a mortgage. They look at things like whether you’ve paid bills on time and if you have other large borrowings, such as business loans, credit cards, and car finance. They can also access past borrowings on this report.

The details in your credit report can impact the lender’s decisions, such as offering you a loan.

Publisher: Source link

{kind=link}