Bowen Xiao

Zero-day options have exploded in popularity in recent years, accounting for approximately half of S&P 500’s total options volume, a ten-fold increase from just 5% in 2016. Their flexibility, low premia and underlying leverage appeal to all market participants ranging from conservative investors hedging against intraday market volatility to aggressive traders speculating for quick profit generation. The rapid rise of zero-day options and the memory of a market stress episode known as ‘Volmageddon‘ raises concerns that zero-day options could lead to a similar event. There are differing views among participants on the perceived risks of zero-day options. This post aims to provide a balanced overview.

The rise of zero-day options

Zero-day options are options contracts that are set to expire at or before the end of the trading day. They can be used to take positions on intraday market movements, or to conduct targeted hedging with a greater degree of precision. Market participants write zero-day options or sell options on their last day to capture the remaining premium given the low likelihood of significant unexpected intraday market movement.

Two factors have contributed to this booming popularity – the longstanding efforts by Chicago Board Options Exchange (CBOE) to encourage greater retail participation in S&P 500 options and the increase in risk-taking behaviour especially among retail investors. To date, the increase in zero-day options trading has been mainly observed in CBOE options trade, since this is the largest global equity options market. It is yet to be seen whether similar developments will be observed in the UK or elsewhere.

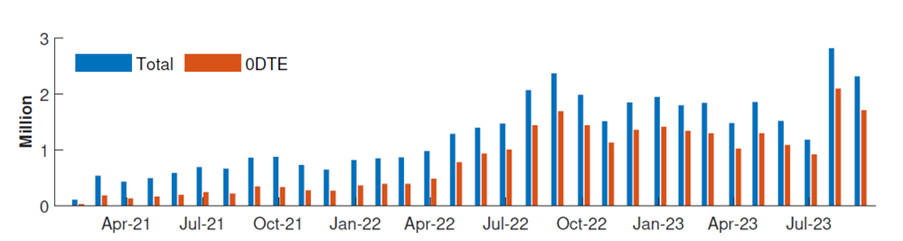

Financial market expansion

In February 2021, CBOE activated the ‘Automated Improvement Mechanism‘ to incentivise greater participation in S&P 500 options by providing execution and price improvements for smaller order sizes. This also enhanced market liquidity as marker-makers generally prefer smaller order sizes due to their ease to hedge. In May 2022, CBOE expanded S&P 500 options expiration days from three to all five weekdays. Although this impacted all options, the effect on zero-day options trading is evident as can be seen in Figure 1. CBOE estimated that 49% of S&P 500 options trading today are using zero-day options.

Figure 1: Total S&P 500 options trading volume by Time to Expiry (2016 to August 2023)

Source: CBOE article: The Evolution of Same Day Options Trading, 3 August 2023.

The improved market conditions have encouraged both market participation and innovation. The first zero-day options exchange-traded fund was launched in September 2023, tracking the performance of the Nasdaq100 Index. Since then, multiple zero-day options-based products have come to the market tracking the price movement of stock indexes, commodities, and US treasury bond of different maturities. This trend suggests that more innovative zero-day options-based investment products could come to the market in the future.

Booming retail popularity

The trading boom since the meme stock craze and the leveraged nature of options have led to a surge in retail speculation. It is estimated that zero-day options represent over 75% of all retail S&P 500 options trade (see Figure 2 from Beckmeyer et al (2023)), and CBOE estimated over 30% of S&P 500’s total zero-day options volume is retail.

Figure 2: Retail S&P 500 options monthly trading volume

Source: Beckmeyer et al (2023), Retail Traders Love 0DTE Options… But Should They?.

The distinctive characteristics of zero-day options – a low nominal price, frequent expiration cycle and rapid outcome realisation – appeal to retail speculators who strongly prefer a high-risk and high-return lottery-like instrument. While trading zero-day options appear cheaper on paper, the cost could quickly accumulate. Beckmeyer et al (2023) estimated that approximately 60% of retail traders’ daily losses in zero-day options trading are due to transaction cost.

Potential risks with zero-day options

The surge in popularity, market speculators and related investment vehicles have raised concerns that zero-day options could create systemic risks by exacerbating market volatility. I briefly examine four risks introduced by zero-day options:

- Significant intraday movements would lead to market-makers making larger positional adjustments to neutralise their exposure. Due to their shorter time-to-expiration, zero-day options are highly sensitive to market movements. The hedging intensity necessitated to neutralise zero-day options exposure requires market-makers to constantly transact in the underlying market. The frequency of hedging required could exacerbate volatility of the underlying market and result in a loop that magnifies the initial market impact.

- The risk of zero-day options may not be limited to just the underlying market associated with the contract. The asset holding and hedging strategy of financial institutions could cause volatilities in the zero-day options market to ripple-through other asset classes. For example, if financial institutions use a portfolio of short-term liquid assets as collateral against their options exposure, significant intraday movements could force the liquidation of these holdings and amplify the volatility and liquidity pressure in other markets.

- Potential deficiencies in the current margining system, and the inability of risk management infrastructure to keep pace with new market developments. The current margining system for both centrally and non-centrally cleared derivatives typically operate on a daily cycle, with margins collected at least once per day based on end-of-day positioning. For centrally cleared derivatives, central counterparties can call for intraday collateral via either scheduled or ad-hoc calls, but since traders open and exit multiple zero-day option positions during the day, it’s unclear to which extent the current margining requirement captures these activities. In a market stress, the intraday accumulation of unrealised losses could expose financial institutions with insufficient margin protection. Additionally, risk management infrastructures are generally designed around the daily margining process, raising concerns about insufficient intraday risk management.

- Intraday risks are not captured explicitly under the Pillar 1 market risk regime, and thus the Pillar 1 market risk capital requirement may not be sufficiently prudent for institutions engaging in zero-day options trading. The current Pillar 1 market risk regime uses end-of-day positioning to assess capital requirement, with potential deficiencies in risk assessment and capital shortfall addressed in the bank-specific Pillar 2 capital requirement. Since intraday risks are not explicitly assessed in Pillar 1 capital evaluations, relying solely on institutions to upgrade their risk management infrastructures without a prudential backstop may be insufficient to safeguard the financial system against future crisis.

Market’s concerns of zero-day options

There are concerns in the market that unforeseen risks in zero-day options could trigger the next financial crisis, but many do not share the same sentiment.

Potential imbalances between traders and market-makers and market-makers desire to maintain a neutral exposure could exacerbate market volatility. JP Morgan warned that the unwinding of zero-day options could generate sharp market swings and has the potential to transform a 5% S&P 500 intraday market decline into 25%. A recent academic study found that zero-day options trading has a significantly higher impact on intraday volatility than trading other options. A separate study also stated that increased zero-day options trading is associated with increased intraday volatility, but the current trading demand for zero-day options has resulted in market-makers hedging in the direction that mitigates market volatility. Therefore, if market-makers’ net zero-day options position is large enough, the attenuating effect can fully offset or even reverse the increase in market volatility caused by zero-day options trading.

Furthermore, since zero-day options have no overnight risk, market participants believe they are unlikely to accumulate systemic risks to the level that could cause significant market disruption. Also, institutions remain the main driver of zero-day options demand, and the netting effect of institutions’ multi-leg trades could also alleviate some of the impact that zero-day options trading may have on market volatility. In September 2023, CBOE reassured the market that despite the huge notional daily trading volume, the actual net exposure for zero-day options market-makers is fairly negligible, with average net gamma ranging from 0.04% to 0.17% of the daily S&P futures liquidity. Moreover, CBOE observed no discernible impact on market volatility from zero-day options trading.

During the rapid market sell-off on 5 August 2024, zero-day options’ trading volume declined significantly to 26% of S&P 500’s total options volume from a yearly average of 48%. A Bloomberg article quotes a note by Bank of America stating that the concerns of zero-day options contributing to the rise in equity volatility are ‘largely misguided or at minimum greatly overstated’. Market analysts believe pricing difficulties in a highly volatile market and the preference for longer-dated options to hedge against uncertain market or economic conditions led to traders refraining from trading zero-day options. As the market recovers, zero-day options subsequently returned to their usual volume.

Conclusion

Innovation will continue to shape the financial market and new risks will emerge as the market evolves. I recognize the concerns that these shorter-dated options have the potential to introduce unforeseen risks, but given that the market has only been experiencing zero-day options at a higher volume since 2022, a lack of data and history makes it difficult to assess the materiality of these risks. Institutions are responsible for adequately managing their risk exposure, but there may be a case for broader risk assessment in the future.

Bowen Xiao works in the Bank’s Banking Capital Policy Division.

If you want to get in touch, please email us at [email protected] or leave a comment below.

Comments will only appear once approved by a moderator, and are only published where a full name is supplied. Bank Underground is a blog for Bank of England staff to share views that challenge – or support – prevailing policy orthodoxies. The views expressed here are those of the authors, and are not necessarily those of the Bank of England, or its policy committees.

Share the post “Zero-day options and financial market vulnerability”

Publisher: Source link

{kind=link}

{kind=link}

{kind=link}